All Categories

Featured

Table of Contents

For many people, the largest problem with the boundless financial idea is that first hit to early liquidity brought on by the costs. Although this con of unlimited banking can be decreased significantly with correct plan design, the initial years will always be the most awful years with any Whole Life plan.

That claimed, there are specific boundless financial life insurance coverage policies developed mostly for high early money value (HECV) of over 90% in the first year. The long-term efficiency will usually considerably delay the best-performing Infinite Financial life insurance policy plans. Having accessibility to that extra 4 numbers in the first couple of years might come at the price of 6-figures down the road.

You in fact obtain some significant long-lasting advantages that help you recoup these early costs and after that some. We find that this prevented early liquidity problem with limitless banking is more psychological than anything else as soon as thoroughly explored. As a matter of fact, if they definitely required every cent of the cash missing from their infinite financial life insurance policy in the initial couple of years.

Tag: unlimited financial idea In this episode, I discuss financial resources with Mary Jo Irmen who educates the Infinite Banking Principle. This subject might be debatable, yet I want to obtain diverse views on the show and learn more about different strategies for ranch monetary administration. Some of you may agree and others won't, however Mary Jo brings an actually... With the increase of TikTok as an information-sharing platform, financial guidance and approaches have actually located an unique way of spreading. One such technique that has actually been making the rounds is the unlimited financial concept, or IBC for short, amassing endorsements from celebrities like rap artist Waka Flocka Flame. While the approach is currently prominent, its origins trace back to the 1980s when financial expert Nelson Nash introduced it to the world.

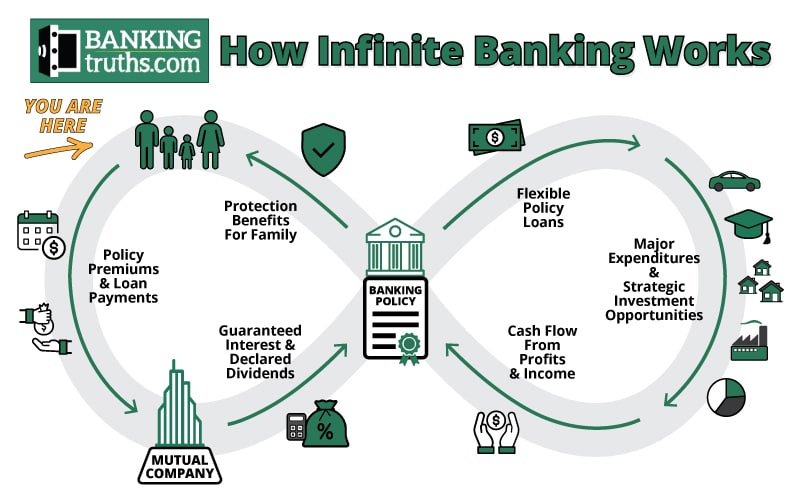

Within these plans, the cash value expands based upon a price established by the insurance provider. As soon as a substantial cash worth gathers, insurance policy holders can obtain a money value lending. These car loans differ from traditional ones, with life insurance policy working as collateral, suggesting one can lose their coverage if loaning excessively without sufficient money value to sustain the insurance coverage expenses.

And while the appeal of these policies appears, there are inherent limitations and dangers, requiring diligent money value tracking. The method's authenticity isn't black and white. For high-net-worth people or company owner, especially those utilizing strategies like company-owned life insurance coverage (COLI), the advantages of tax breaks and compound development can be appealing.

Infinite Banking Concept Videos

The attraction of unlimited financial does not negate its obstacles: Expense: The fundamental demand, a permanent life insurance policy plan, is costlier than its term equivalents. Qualification: Not everybody receives whole life insurance policy as a result of strenuous underwriting procedures that can exclude those with specific health and wellness or lifestyle conditions. Complexity and risk: The complex nature of IBC, combined with its risks, might deter numerous, particularly when easier and less dangerous alternatives are available.

Alloting around 10% of your regular monthly income to the plan is simply not viable for many people. Part of what you read below is simply a reiteration of what has actually already been claimed over.

So prior to you get yourself right into a scenario you're not gotten ready for, understand the following first: Although the idea is generally marketed therefore, you're not really taking a lending from on your own. If that held true, you would not have to repay it. Rather, you're obtaining from the insurer and have to settle it with interest.

Some social media blog posts advise using money value from whole life insurance policy to pay down credit rating card financial debt. When you pay back the lending, a section of that interest goes to the insurance coverage business.

For the initial several years, you'll be settling the commission. This makes it very tough for your policy to accumulate worth throughout this moment. Entire life insurance policy costs 5 to 15 times more than term insurance policy. Many individuals merely can not manage it. So, unless you can afford to pay a few to a number of hundred dollars for the following years or more, IBC won't help you.

Infinite Banking Examples

Not everyone ought to count exclusively on themselves for financial protection. If you need life insurance policy, below are some useful ideas to take into consideration: Consider term life insurance policy. These policies supply coverage during years with considerable monetary obligations, like home loans, pupil loans, or when looking after young youngsters. Ensure to go shopping around for the ideal price.

Copyright (c) 2023, Intercom, Inc. () with Reserved Font Call "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Booked Font Style Call "Montserrat".

Infinite Banking Concept Review

As a CPA focusing on realty investing, I've brushed shoulders with the "Infinite Banking Concept" (IBC) more times than I can count. I have actually even spoken with professionals on the subject. The main draw, apart from the apparent life insurance policy advantages, was always the idea of accumulating money worth within a long-term life insurance plan and borrowing versus it.

Sure, that makes good sense. Honestly, I constantly assumed that cash would certainly be better invested straight on investments rather than channeling it with a life insurance coverage policy Till I uncovered just how IBC might be integrated with an Irrevocable Life Insurance Coverage Trust Fund (ILIT) to produce generational riches. Let's begin with the fundamentals.

Infinite Banking Insurance Agents

When you borrow against your plan's cash money value, there's no set payment routine, providing you the liberty to take care of the lending on your terms. On the other hand, the cash money worth remains to grow based upon the policy's guarantees and rewards. This configuration allows you to accessibility liquidity without disrupting the long-lasting growth of your policy, gave that the funding and passion are handled carefully.

As grandchildren are birthed and expand up, the ILIT can purchase life insurance coverage policies on their lives. Family members can take loans from the ILIT, making use of the money worth of the plans to fund financial investments, begin companies, or cover significant expenses.

An essential element of handling this Household Financial institution is making use of the HEMS criterion, which represents "Health, Education, Maintenance, or Support." This guideline is often consisted of in count on agreements to guide the trustee on just how they can distribute funds to beneficiaries. By adhering to the HEMS criterion, the trust ensures that circulations are created crucial requirements and long-lasting support, securing the count on's assets while still offering relative.

Raised Adaptability: Unlike stiff small business loan, you regulate the settlement terms when obtaining from your very own policy. This enables you to framework settlements in such a way that lines up with your company cash money flow. infinite banking videos. Improved Capital: By financing overhead through plan lendings, you can possibly liberate cash money that would otherwise be bound in typical finance repayments or devices leases

He has the exact same devices, but has also developed additional cash value in his plan and obtained tax benefits. And also, he currently has $50,000 offered in his policy to use for future opportunities or costs., it's essential to see it as more than just life insurance.

What Is Infinite Banking Life Insurance

It's concerning creating a flexible financing system that offers you control and offers numerous advantages. When made use of purposefully, it can enhance other investments and organization strategies. If you're intrigued by the possibility of the Infinite Banking Idea for your organization, below are some actions to take into consideration: Inform Yourself: Dive much deeper into the idea via reputable publications, workshops, or assessments with knowledgeable professionals.

{kind=link}

Latest Posts

Why You Should Consider Being Your Own Bank

Infinite Banking - Be Your Own Bank - Insure U4 Life

Nelson Nash Bank On Yourself